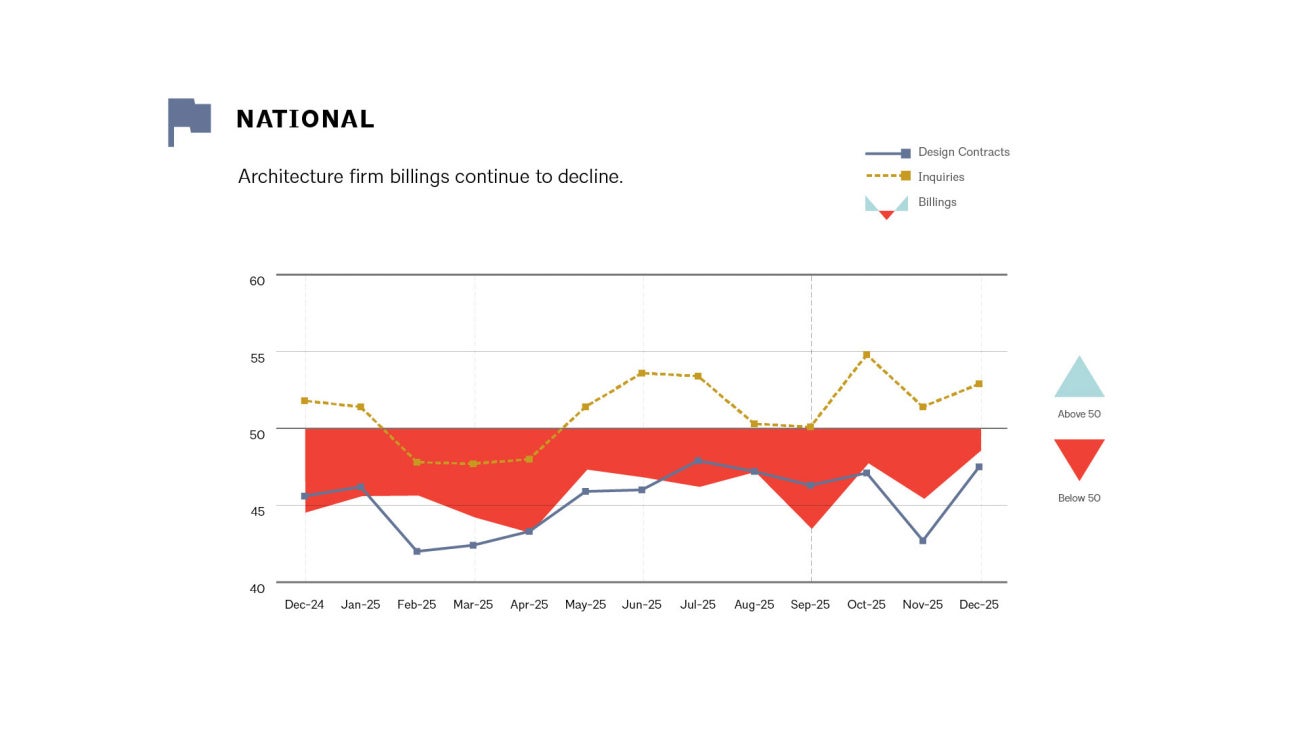

The AIA/Deltek Architecture Billings Index® (ABI) ended 2025 in negative territory, with December recording a score of 48.5, improving from 45.3 in November. While the rise indicates that fewer firms reported a decline in billings, the index remains below the critical 50-point threshold, confirming that overall billings are still contracting.

Architecture firm billings declined throughout 2025, continuing a downtrend seen in most months since October 2022. And despite the softer pace of decline in December, lower design contract values suggest that a near-term rebound remains unlikely.

Still, the market is not without stabilizers. Backlogs remain strong, averaging 6.3 months, helping firms maintain operational continuity even as new opportunities become more difficult to secure. Larger firms with annual billings of $5 million or more report significantly deeper backlogs of 8.6 months, while institutional specialists average 8.2 months, reinforcing the role of long-cycle sectors in keeping pipelines active.

Regionally, performance remains uneven. The Midwest posted the only positive reading at 51.7, marking its fourth consecutive month of growth, while all other regions remained below 50: South (47.7), West (45.3), and Northeast (44.2).

Across market segments, declines continued, with multifamily residential seeing the steepest drop at 45.5. Institutional work held up better at 48.7, followed by commercial/industrial (47.8) and mixed practice (44.0).

Forward indicators were mixed: project inquiries rose to 52.9, but the design contracts index stayed weak at 47.5, confirming slower conversions from interest to signed work as 2026 begins.

Source: AIA with additional information added by Glass Balkan