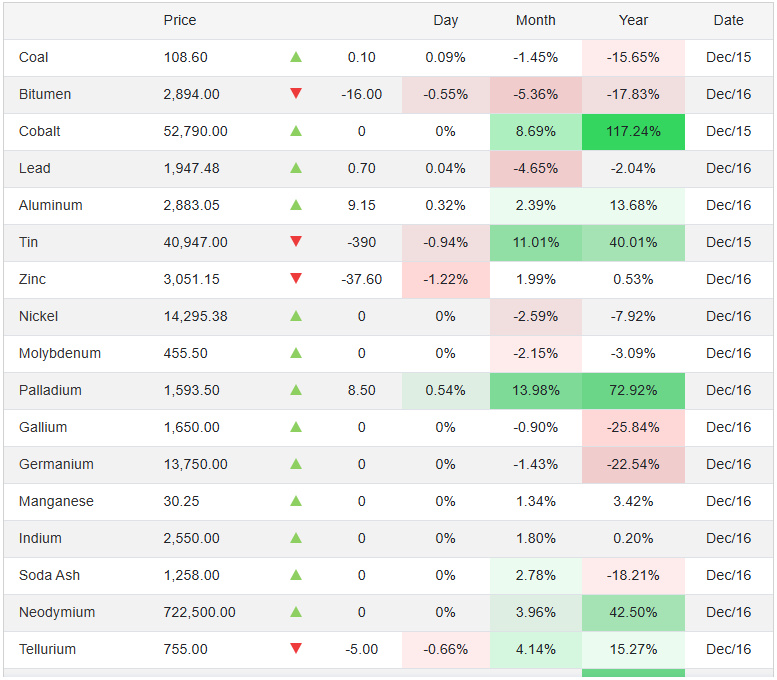

Aluminum prices have remained firm in December 2025, reflecting a market shaped by tightening global supply and cautiously improving demand prospects. Aluminum futures traded in the UK have hovered around $2,870 per tonne, close to the one-month high reached on December 5, as supportive macroeconomic signals offset lingering concerns over global growth.

So far this year, aluminum prices have risen by nearly 14%, placing the metal among the stronger performers in the base metals complex. Year-on-year, prices are up by approximately 9–10%, underlining the sustained pressure on supply chains and the importance of policy signals from major producing regions.

China, which accounts for almost 60% of global aluminum output, remains central to market dynamics. Recent indications of additional stimulus measures aimed at stabilizing the country’s property sector have lifted expectations for increased demand for industrial metals. Construction, infrastructure, transportation, and packaging remain core end-use sectors for aluminum, making any recovery in real estate activity particularly relevant for consumption levels.

At the same time, supply growth remains constrained. China is expected to approach its government-mandated annual production cap of 45 million tonnes, leaving little room for further expansion. This structural limit has become a key factor supporting prices, as incremental demand cannot easily be met through higher Chinese output.

Outside China, supply challenges continue to emerge. Plans to build new aluminum smelters in Indonesia have faced repeated delays, largely due to high energy costs and regulatory hurdles, slowing the pace of new capacity coming online. Additional pressure has come from operational disruptions elsewhere, including the suspension of one potline at Iceland’s Grundartangi smelter following equipment failure, temporarily reducing output in the European market.

In recent weeks, aluminum prices have traded within a relatively narrow range, fluctuating between approximately $2,775 and $2,920 per tonne, with the upper end of the range marking the strongest levels seen since late 2022. Trading Economics models currently project aluminum prices to average around $2,919 per tonne by the end of the current quarter, suggesting continued firmness if supply constraints persist.

Aluminum futures are primarily traded on the London Metal Exchange (LME), alongside contracts on COMEX in New York and the Shanghai Futures Exchange. The standard aluminum futures contract represents five tonnes of metal, and LME pricing remains the global benchmark for producers, processors, and end-users.

From a broader perspective, aluminum remains a strategically important material for multiple industries, including aerospace, automotive manufacturing, packaging, rail transport, and construction. Major global producers include Chalco, Alcoa, Rio Tinto, UC Rusal, Norsk Hydro, Xinfa, and South32, while the world’s largest bauxite reserves, aluminum’s primary raw material, are located in Australia, China, and Guinea.

While short-term volatility remains a feature of the market, the combination of restricted production growth, ongoing smelter challenges, and signs of demand stabilization continues to underpin aluminum prices as 2025 draws to a close.

Source: tradingeconomics.com with additional information added by Glass Balkan