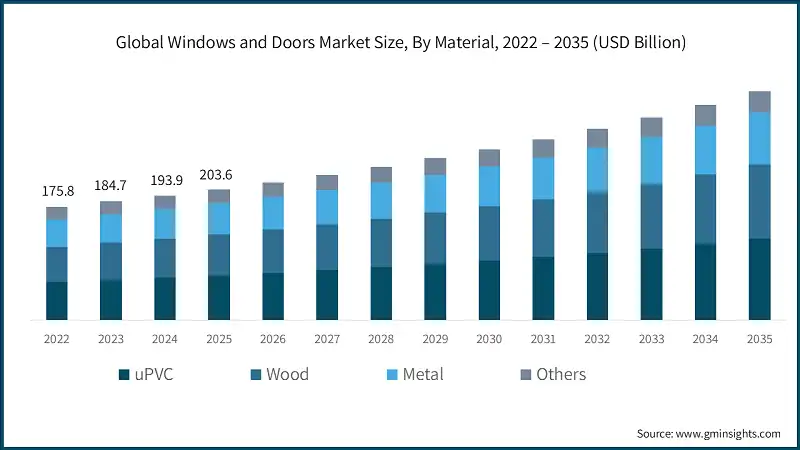

The global windows and doors market is undergoing a significant transformation, moving beyond traditional building components toward high-performance, energy-efficient, and technologically advanced solutions. According to Global Market Insights, the market was valued at USD 203.6 billion in 2025 and is projected to reach USD 355.1 billion by 2035, registering a 5.8 % CAGR between 2026 and 2035. This growth reflects not only the expansion of global construction but also the evolving demands of homeowners, architects, and developers who increasingly prioritize efficiency, sustainability, and smart technology.

Energy Efficiency and Regulation Driving Innovation

A major driver of market growth is the rise of energy-efficient products in response to stricter building codes and sustainability regulations. In North America, programs like ENERGY STAR Version 7.0 push for lower thermal loss and better insulation, while the European Union’s Energy Performance of Buildings Directive (EPBD) is accelerating adoption of high-performance windows and doors. Features such as triple-pane glass, low-emissivity (Low-E) coatings, and thermally broken aluminum frames are becoming standard, delivering improved energy performance and reducing carbon footprints.

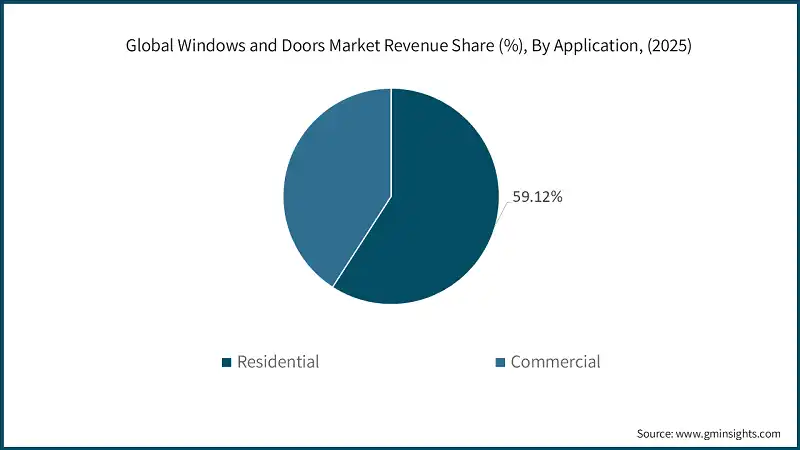

Urbanization and Renovation Boost Demand

Rapid urbanization across Asia-Pacific markets, including China and India, is fuelling demand for new residential and commercial construction. Simultaneously, in mature markets like North America and Europe, aging building stock is prompting renovation and replacement cycles. Homeowners and developers are increasingly seeking modern, durable, and aesthetically appealing fenestration products, creating a steady stream of opportunities for industry players.

Smart and Connected Products Enter the Mainstream

The windows and doors sector is embracing smart home integration. IoT-enabled solutions, automated operation, predictive maintenance, and remote monitoring are no longer niche features; they are increasingly essential in high-end residential and commercial developments. This trend is particularly evident in Europe and North America, where premium products combine energy efficiency with intelligent functionality, meeting both regulatory and consumer demands.

Industry Leaders and Competitive Landscape

The market remains competitive and concentrated, led by global giants including Andersen Corporation, JELD-WEN Inc., Pella Corporation, LIXIL Corporation, and Schüco International KG. Andersen holds roughly 12 % market share in 2025, while JELD-WEN and Pella dominate the North American residential segment. Schüco and LIXIL are leaders in high-performance European and Asia-Pacific markets, respectively. Collectively, these companies accounted for nearly 30 % of the global market in 2025, illustrating both the scale and competitiveness of the industry.

Material Trends and Regional Dynamics

Material innovation is reshaping the market. Aluminum remains dominant in commercial construction for its strength and recyclability, while uPVC and composite materials are rapidly expanding in residential projects for their cost-efficiency and thermal performance. Regionally, Asia-Pacific is the fastest-growing market, driven by infrastructure expansion and urbanization, while North America and Europe focus on energy efficiency upgrades and renovation projects.

Despite strong growth, challenges remain: supply chain volatility for aluminum, glass, and PVC, along with high upfront costs for premium and smart solutions, could limit adoption in price-sensitive markets. Yet opportunities abound in sustainable materials, automated manufacturing, and digital integration, which are redefining value chains and creating new revenue streams.

The windows and doors market is no longer just about materials; it is a hub of innovation, regulation-driven design, and smart technology adoption. Companies that embrace performance, sustainability, and connectivity are poised to lead the next decade of growth.

Source: gminsights.com with additional information added by Glass Balkan