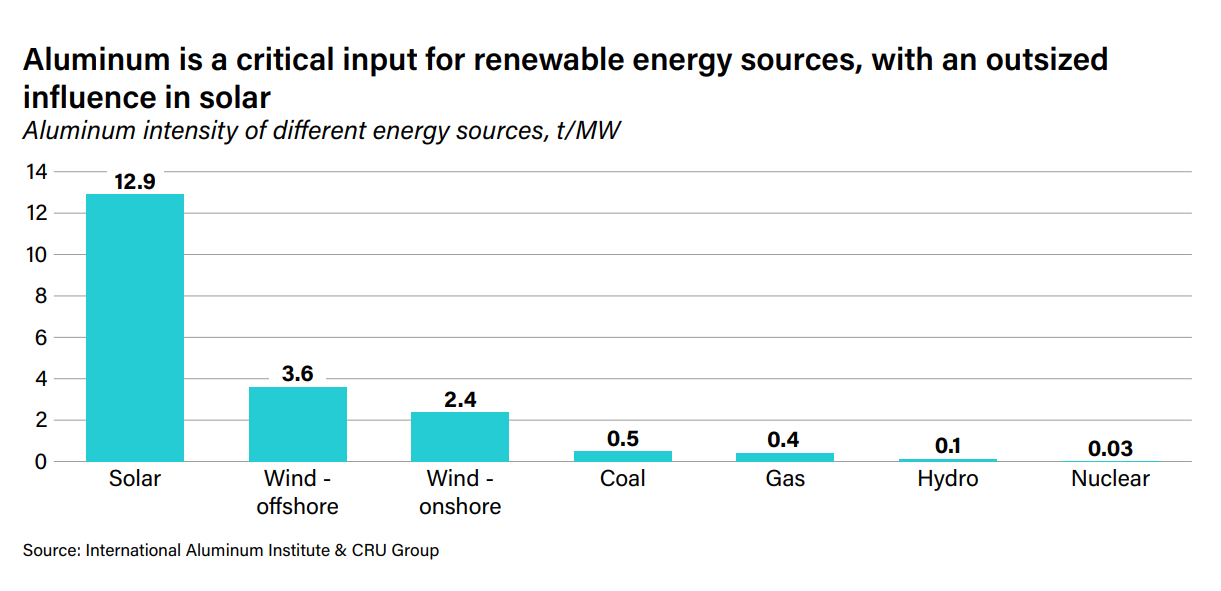

Alcoa and Eurasia Group’s white paper, “Competitiveness & Green Transition in the Aluminum Industry: Finding Synergies or Facing Trade-Offs,” highlights aluminum’s essential role in the global energy transition. The metal is critical for renewable energy technologies, particularly solar, while the industry works to reduce its own carbon footprint.

Global aluminum demand is projected to grow 80% by 2050, driven by decarbonization across multiple sectors. The industry currently accounts for around 3% of global industrial carbon emissions. Nicol Gagstetter, Alcoa’s EVP and Chief External Affairs Officer, emphasizes the need to align competitiveness with ambitious decarbonization goals.

Regional progress varies: Europe leads with advanced carbon markets and policy frameworks, Latin America and Australia advance clean energy integration, while Asia and the Gulf lag. China and India remain heavily coal-dependent, while Gulf nations plan gigawatt-scale renewable projects.

The sector has shown strong leadership through collaborative platforms like the Mission Possible Partnership, the International Aluminium Institute, and the First Movers Coalition. Alcoa powers 86% of its smelters with renewable energy, and net-zero aligned aluminum projects tripled in 2024. Buyers are committing to procure at least 10% of primary aluminum from near-zero emissions processes by 2030.

Challenges remain, including slow permitting, long project timelines, and rising grid costs, particularly in the US and EU. To stay competitive, producers are decarbonizing secondary aluminum, enhancing supply chain traceability, and leveraging policy differences. These strategies enable the aluminum industry to grow while supporting a low-carbon future.

Source: Eurasia Group with additional information added by Glass Balkan